Property tax planning for a luxury Amelia Island purchase is defined as the deliberate structuring of ownership, exemptions, and entity design before closing to reduce your annual tax burden and protect long-term investment value. Florida's tax code rewards buyers who plan ahead, and Nassau County's local rules add a second layer of complexity that catches many affluent buyers off guard. The strategies available here, from Florida's Homestead Exemption and LLC structuring to cost segregation and 1031 exchanges, can mean the difference between a property that performs and one that quietly erodes wealth. We believe that understanding these tools before you sign is not optional. It is the foundation of smart ownership on this island.

What are the key Florida property tax provisions affecting luxury Amelia Island homes?

Florida's Homestead Exemption is the most consequential tax provision for any primary residence buyer on Amelia Island. The current exemption reduces taxable assessed value by $50,000 for qualifying primary residences, and Governor Ron DeSantis has proposed phased increases that would push that figure to $250,000 and eventually $500,000. If enacted, the proposal would exempt 92% of homesteaded properties from property tax entirely, shifting a meaningful share of the tax burden to second homes, investment properties, and luxury vacation residences. For buyers purchasing on Amelia Island as a second home or seasonal retreat, this shift matters directly.

The exemption carries strict eligibility rules. You must establish the property as your permanent, primary Florida residence and apply with the Nassau County Property Appraiser by March 1 of the tax year. Missing that deadline means waiting a full year to qualify. Beyond the basic exemption, Florida's Save Our Homes cap limits annual increases in assessed value to 3% or the rate of inflation, whichever is lower, providing compounding protection over time for primary residents.

For luxury second homes, the picture is different. These properties receive no Homestead Exemption and no Save Our Homes protection, meaning their assessed values can reset to full market value at each sale. On a $3 million or $5 million Amelia Island property, that reset can translate to a significant annual tax increase compared to what the prior owner paid. Understanding this dynamic before you make an offer is a core part of planning for luxury home purchases.

Key provisions to track before closing include:

- Homestead Exemption deadline: March 1 application with the Nassau County Property Appraiser

- Save Our Homes cap: Limits assessed value increases to 3% annually for qualifying primary residences

- Proposed exemption increases: Phased increases to $250,000 and $500,000 could shift tax burdens significantly to non-homesteaded luxury properties

- Assessment reset at sale: Second homes and investment properties are reassessed at full market value upon transfer

- Appeals window: Buyers can contest assessed values through the Nassau County Value Adjustment Board within a defined annual window

Pro Tip: Request the prior owner's tax bill and the current assessed value from the Nassau County Property Appraiser before making an offer. The gap between assessed value and purchase price tells you exactly how much your annual tax bill may increase at closing.

How do Amelia Island's local tax rules and rental regulations influence property tax planning?

Nassau County's local tax rules add a layer of obligation that goes well beyond the state framework. If you plan to generate rental income from your Amelia Island property, even occasionally, you must understand how those activities interact with your tax status and compliance calendar.

-

Tourist Development Tax compliance. Nassau County enforces a 5% Tourist Development Tax on all transient accommodations rented for six months or less. This tax applies whether you manage the rental yourself or list through Airbnb or Vrbo. Many owners are unaware that the obligation to remit this tax rests with the property owner, not the platform. Hiring a local property manager who handles remittance is the most reliable way to stay compliant.

-

Zoning and permit requirements. Fernandina Beach enforces short-term rental permits in specific zones, including a Resort Rental Dwelling Permit requirement in R-3 zoning. Properties in other zones may require a minimum 30-day rental duration. Buying within Fernandina Beach city limits versus unincorporated Nassau County creates distinct regulatory obligations, and confirming your parcel's jurisdiction before purchase is non-negotiable.

-

Homestead exemption and rental conflict. Renting out a homesteaded property is treated as abandonment of homestead status under Florida law. This is one of the most overlooked risks for dual-use luxury homes. If you claim the Homestead Exemption and then rent the property, even for a single season, you risk losing the exemption entirely and triggering a reassessment.

-

Payment calendar and delinquency. Nassau County property taxes are due annually by March 31, with delinquency beginning April 1. Early payment discounts are available before March 1. On a high-value property, these discounts are worth capturing, and missing the deadline carries penalties that compound quickly.

-

Audit and reassessment risk. Renting a homesteaded property can trigger a tax audit or reassessment that revokes the exemption retroactively. The financial exposure from a retroactive reassessment on a multi-million-dollar property is substantial and entirely avoidable with proper planning.

Pro Tip: If you intend to use your Amelia Island property as both a primary residence and an occasional rental, consult a Florida tax attorney before closing. The homestead exemption and rental income are structurally incompatible, and the cost of losing the exemption far exceeds most short-term rental revenue.

What ownership structures and investment strategies optimize tax benefits for luxury Amelia Island purchases?

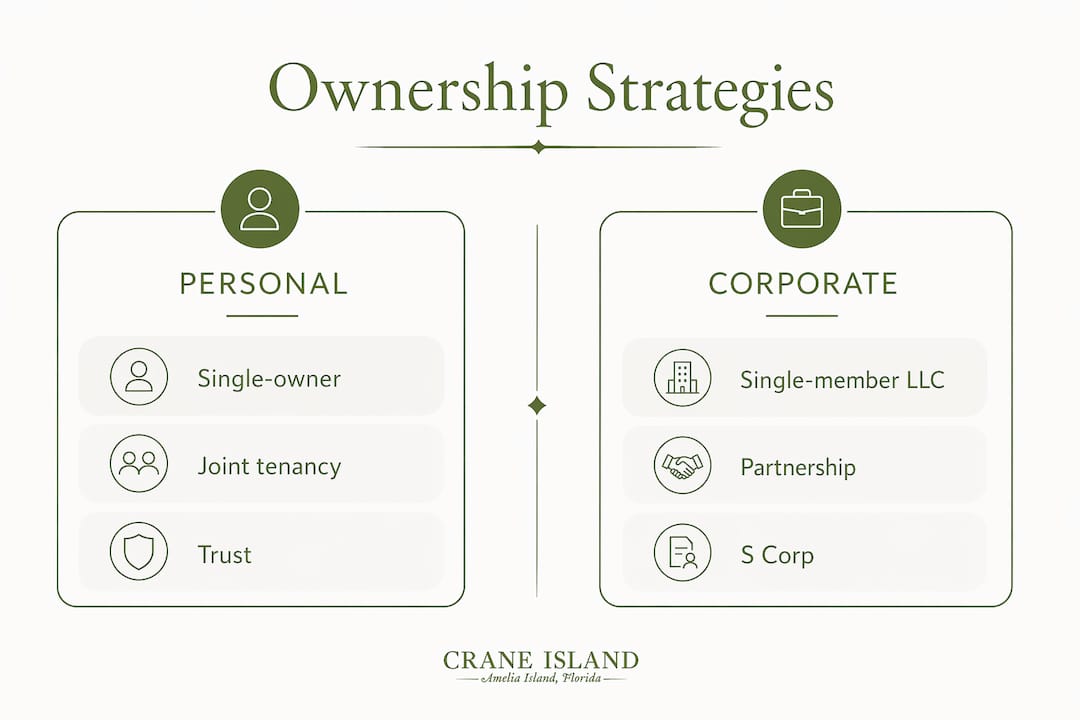

The most effective ownership structure for a luxury Amelia Island investment property is rarely a personal name. Holding luxury properties in personal name is discouraged for high-net-worth buyers because it exposes personal assets to liability and forfeits the tax flexibility that entity structures provide. Multi-entity structures using LLCs, family limited partnerships, or irrevocable trusts give buyers both asset protection and meaningful control over how income, depreciation, and eventual sale proceeds are taxed.

| Structure | Primary benefit | Best suited for |

|---|---|---|

| Single-member LLC | Liability protection, pass-through taxation | Investment or rental properties |

| Multi-member LLC | Income splitting, estate planning flexibility | Family ownership or partnerships |

| Irrevocable trust | Estate tax reduction, generational transfer | Long-term legacy properties |

| Family limited partnership | Valuation discounts, gift tax efficiency | Multi-property portfolios |

Cost segregation is the most powerful accelerated depreciation tool available for luxury property investors. Rather than depreciating a property over the standard 27.5-year residential schedule, a cost segregation study reclassifies components like flooring, cabinetry, landscaping, and specialty systems into 5-year, 7-year, or 15-year categories. On a $4 million Amelia Island home, this reclassification can generate hundreds of thousands of dollars in accelerated deductions in the first few years of ownership. That deduction offsets ordinary income, making cost segregation particularly valuable for buyers with significant W-2 or business income.

A unified advisory team coordinating your CPA, estate attorney, and real estate advisor before closing produces far better outcomes than assembling advisors after the fact. The ownership structure you choose at purchase determines your depreciation basis, your estate tax exposure, and your eligibility for a 1031 exchange when you eventually sell. Changing structures after closing is possible but costly. Getting it right at the outset is the standard practice among sophisticated investors.

Pro Tip: Commission a cost segregation study within the first year of ownership. The IRS allows a catch-up deduction in the year the study is completed, meaning buyers who purchased in prior years can still benefit without amending returns.

How to integrate property tax planning with due diligence on Amelia Island

Effective property tax planning begins during due diligence, not after closing. Amelia Island's geography and regulatory environment create specific risks that directly affect both your tax obligations and your carrying costs. Careful due diligence on flood risk, zoning, and historic district requirements is critical before purchasing luxury property here, and each of these factors connects to your tax picture in ways that are easy to miss.

Flood zone classification determines your insurance costs, which are a direct ownership expense. Properties in FEMA Special Flood Hazard Areas carry mandatory flood insurance requirements that can add thousands of dollars annually to your cost basis. Nassau County flood maps are publicly available, and reviewing them before making an offer is a basic step that many buyers skip.

Historic district designation in Fernandina Beach adds a layer of review that affects renovation costs and timelines. Properties within the historic district require a Certificate of Appropriateness before permits are issued, which can delay improvements and affect your depreciation timeline if you are planning a cost segregation study. At the same time, certain historic preservation tax credits may be available for qualifying renovations, creating an incentive worth exploring with your tax advisor.

Parcel jurisdiction matters more than most buyers realize. Fernandina Beach city limits and Nassau County have distinct land-use and tax rules. A property just inside the city line may face historic district review, additional permitting layers, and different millage rates than a comparable property a few blocks away in unincorporated county territory. Confirming jurisdiction before purchase shapes your entire tax and compliance strategy.

Concierge real estate services on Amelia Island simplify this complexity by coordinating tax deadlines, permits, flood insurance, and local compliance under one advisor. For buyers managing multiple properties or relocating from out of state, this model removes the administrative burden that leads to missed deadlines and costly errors. We see this approach as the most practical way to protect both your investment and your time.

Key takeaways

Strategic property tax planning before closing on a luxury Amelia Island purchase protects your investment, reduces annual carrying costs, and prevents costly compliance errors that are difficult to reverse.

| Point | Details |

|---|---|

| Homestead Exemption timing | Apply by March 1 with Nassau County to qualify for the $50,000 exemption and Save Our Homes cap. |

| Rental and homestead conflict | Renting a homesteaded property revokes the exemption and can trigger retroactive reassessment. |

| Entity structuring at purchase | LLCs and trusts provide liability protection and control over depreciation, estate planning, and 1031 exchanges. |

| Cost segregation value | Reclassifying components to 5-15 year schedules generates substantial early deductions on high-value properties. |

| Due diligence scope | Confirm flood zone, parcel jurisdiction, and historic district status before closing to avoid hidden tax and compliance costs. |

Why I think most affluent buyers underestimate local tax complexity on Amelia Island

From my experience working with high-net-worth buyers across Florida's luxury coastal markets, the most common and costly mistake is treating property tax planning as a post-closing task. Buyers spend months selecting the right property, negotiating price, and designing interiors, then hand the tax question to a CPA two weeks before closing. By that point, the ownership structure is often locked in, the homestead eligibility window is misunderstood, and the rental strategy has not been stress-tested against local zoning rules.

Amelia Island is particularly unforgiving in this regard. The interplay between Nassau County's Tourist Development Tax, Fernandina Beach's zoning requirements, and Florida's homestead rules creates a web of obligations that looks simple on the surface and is genuinely complex in practice. I have seen buyers lose their Homestead Exemption in the first year because they rented the property for a single month without understanding the consequences. That is not a tax technicality. On a $4 million property, it is a five-figure annual cost that compounds indefinitely.

The proactive tax planning approach, including preparing a tax context brief for advisors before the deal closes, is the standard I recommend to every buyer I work with. It forces the conversation about ownership structure, rental intent, and estate goals early enough to actually influence the deal. The buyers who do this consistently outperform those who do not, not because they found a loophole, but because they made deliberate decisions instead of default ones.

The concierge real estate model that has emerged on Amelia Island addresses this gap directly. Having one coordinated team manage tax deadlines, permit compliance, flood insurance, and property management removes the fragmentation that leads to errors. It is not a luxury add-on. For a property of this value, it is the responsible way to own.

— John Hillman

How Crane Island supports your tax planning and ownership journey

Crane Island is built around the belief that owning a luxury home on Amelia Island should feel like a privilege, not an administrative burden. With only 14 custom homesites woven into the preserved marshlands and forests along the Intracoastal Waterway, every detail of the ownership experience here is designed with intention. We connect buyers with the legal, tax, and property management expertise they need to structure their purchase correctly from the start. Whether you are exploring our luxury Amelia Island homes or considering a fully custom build through our design-build program, our team is here to make the path from discovery to ownership as clear and rewarding as the island itself.

FAQ

What is the Florida Homestead Exemption for luxury home buyers?

Florida's Homestead Exemption reduces taxable assessed value by $50,000 for qualifying primary residences, with proposed increases that could raise that figure to $500,000. It applies only to your permanent primary residence and requires a March 1 application deadline with the Nassau County Property Appraiser.

Can I rent my Amelia Island home and keep the Homestead Exemption?

No. Renting a homesteaded property is treated as abandonment of homestead status under Florida law, which revokes the exemption and can trigger a retroactive reassessment. Buyers who plan to generate rental income should structure ownership separately from any homestead claim.

What is the Nassau County Tourist Development Tax?

Nassau County imposes a 5% Tourist Development Tax on all short-term rentals of six months or less. The property owner is responsible for remittance regardless of whether the rental is managed through a platform like Airbnb or Vrbo.

How does cost segregation reduce taxes on a luxury Amelia Island property?

Cost segregation reclassifies building components from a 27.5-year depreciation schedule to 5-year, 7-year, or 15-year categories, generating accelerated deductions in the early years of ownership. On a multi-million-dollar property, this strategy can produce substantial reductions in taxable income.

Should I hold my Amelia Island investment property in an LLC?

Yes, for most investment and rental properties. An LLC provides liability protection and tax flexibility that personal ownership does not, and it supports estate planning strategies like 1031 exchanges and trust integration. Consult a Florida tax attorney before closing to select the right structure for your goals. You can also review what makes Amelia Island real estate unique to understand how local factors shape your ownership decisions.