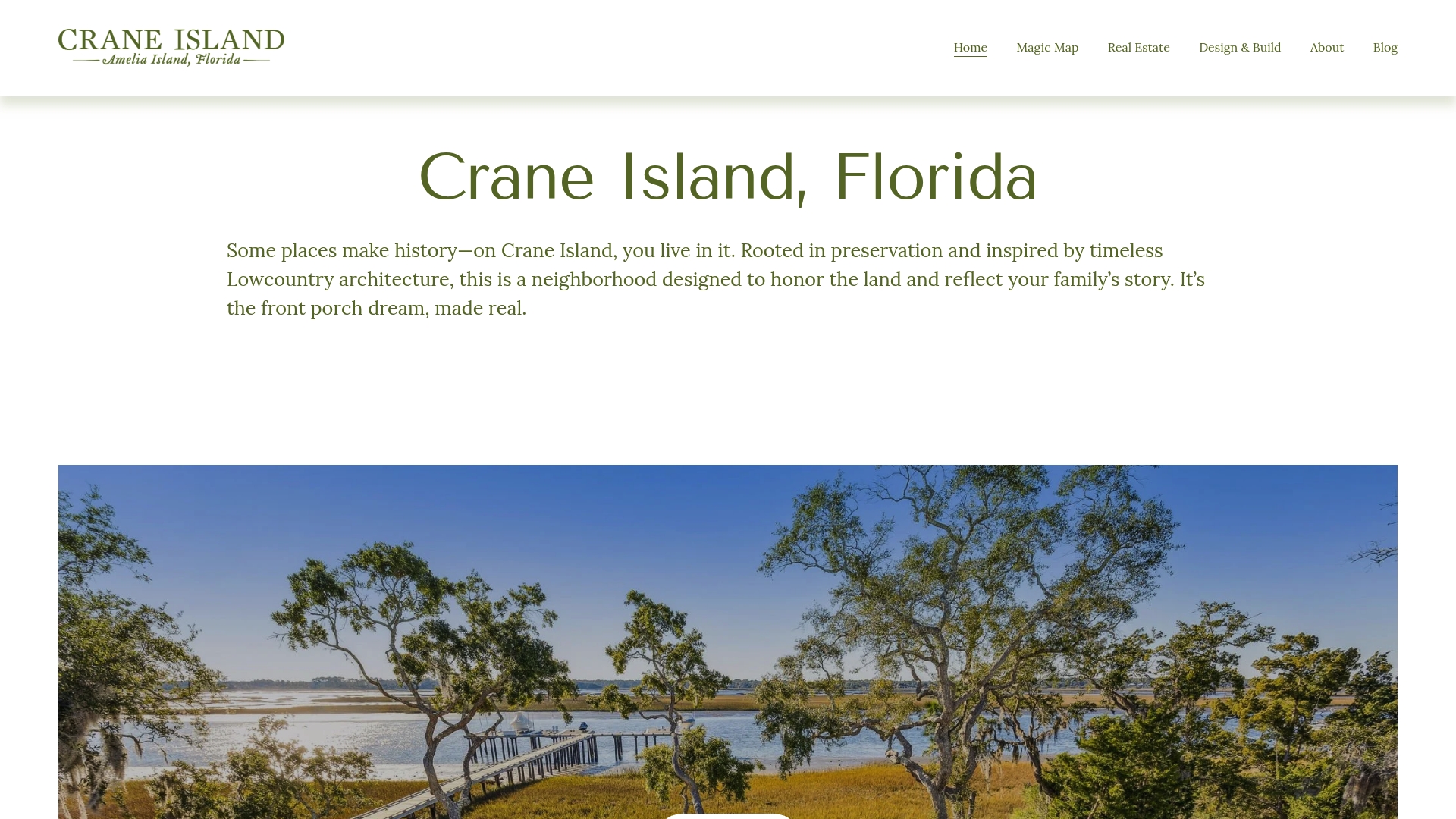

The $2M–$10M luxury real estate segment on Amelia Island is defined by scarcity, micro-location premiums, and a buyer pool that moves on institutional knowledge rather than county-wide averages. Navigating the $2M–$10M Amelia Island market demands more than a strong offer. It requires understanding how oceanfront estates, Intracoastal-facing homesites, and boutique communities each follow their own pricing logic, inventory rhythm, and due diligence requirements. The tools that serve you here include NEFAR transaction reports, FEMA flood-zone maps reviewed parcel by parcel, and comp sets built by neighborhood type rather than ZIP code. This guide gives you the framework to move with confidence in one of Florida's most distinctive coastal markets.

What defines the $2M–$10M Amelia Island luxury market segment

Luxury homes Amelia Island occupy a pricing tier that begins well above the county median and stretches into genuinely rare territory. Island-proper luxury pricing starts around $1M and extends past $3M for oceanfront estates, with the most coveted properties commanding multiples of that figure. Nassau County's median sale price sits near $490,250, a number that reflects a broad market and tells you almost nothing about what a four-bedroom oceanfront estate or a private Intracoastal compound actually trades for.

The segment breaks into three meaningful tiers. Properties in the $2M–$4M range typically include ocean-view estates, larger Intracoastal homes, and well-appointed single-family residences in gated communities. The $4M–$7M band captures true oceanfront parcels, architecturally significant custom builds, and properties with deep-water dock access. Above $7M, you are in a market of genuine one-of-a-kind assets where comparable sales may number in the single digits per year across the entire island.

| Tier | Property type | Typical characteristics |

|---|---|---|

| $2M–$4M | Ocean-view estates, Intracoastal homes | Gated community, 3,000–5,000 sq ft, marsh or water views |

| $4M–$7M | Oceanfront parcels, custom builds | Direct beach access, dock potential, premium finishes |

| $7M–$10M+ | Signature estates | Rare comps, deep-water access, architectural distinction |

Micro-location comp sets built around resort-adjacent, ocean-view, and oceanfront neighborhoods give buyers far better valuation anchors than ZIP-level or county-wide medians. This matters because a buyer relying on Nassau County data to negotiate an oceanfront estate is essentially using the wrong map. Build your comp set around the specific neighborhood type, not the broader geography.

Pro Tip: Ask your agent to pull sold data filtered by neighborhood type and water orientation, not just ZIP code. A marsh-view home and an oceanfront home in the same ZIP code can differ by $1.5M or more.

How does inventory scarcity affect luxury buyers on Amelia Island?

Luxury and oceanfront inventories on Amelia Island are thinner and more volatile than mainstream markets, driven by a high proportion of second-home owners, snowbirds, and short-term rental investors. Nassau County's total active and pending listing count reached 1,088 in April 2026, but that figure includes the full county. The $2M–$10M slice of Amelia Island proper represents a fraction of that pool, and active listings in this tier can drop to a handful at any given time.

Seasonal supply shifts caused by second-home ownership patterns mean that spring and early summer often bring the most visible inventory, while fall listings can represent owners who are genuinely motivated. Days on market at the county level average around 51 days, but luxury properties either sell quickly to well-prepared buyers or sit for extended periods when priced above what micro-location comps support. Neither scenario reflects the county average.

Off-market transactions are a real feature of this segment. Sellers of $5M–$10M properties frequently prefer discretion, and those homes change hands through agent networks before a public listing ever appears. If you are working with an agent who lacks deep local relationships, you may never see the most compelling opportunities.

Strategic approaches to stay competitive in this market:

- Monitor NEFAR MLS data weekly, not monthly, during your active search window

- Ask your agent explicitly about off-market and coming-soon inventory in your target neighborhoods

- Get fully underwritten financing approval before you identify a property, not after

- Track days on market by neighborhood type to identify motivated sellers

- Be prepared to act within 48 to 72 hours when a well-priced listing appears

Pro Tip: Buyers who have toured comparable properties before their target listing appears make faster, more confident decisions. Build familiarity with the market before you need to act.

What due diligence is required for $2M–$10M Amelia Island properties?

Flood risk is the single most consequential due diligence item for any coastal property on Amelia Island, and flood zone designation must be confirmed parcel by parcel, not assumed from neighborhood reputation. Properties in Special Flood Hazard Areas require flood insurance, and lender requirements can significantly affect carrying costs. The difference between a property in AE zone versus X zone can translate to tens of thousands of dollars annually in insurance premiums.

Flood zone labeling alone is not sufficient. A thorough review of the elevation certificate and a comparison of NFIP versus private flood insurance options is critical for underwriting and long-term budgeting. Early-stage verification aligned with your financing timeline prevents last-minute surprises that can derail a closing. Request the elevation certificate from the seller before you finalize your offer, not during the inspection period.

For boutique communities with fewer than ten units, HOA budget scrutiny is more critical than in large-scale developments. When unexpected cost line items divide among six owners rather than sixty, the per-unit impact is severe. Review at least three years of HOA financials, confirm reserve fund adequacy, and understand any pending special assessments before you commit.

| Due diligence item | Responsible party | Timing |

|---|---|---|

| FEMA flood zone confirmation | Buyer's agent or attorney | Before offer submission |

| Elevation certificate review | Licensed surveyor | During inspection period |

| HOA financials and reserves | Buyer's attorney | Within 5 days of contract |

| Seawall and dock inspection | Marine engineer | During inspection period |

| Roof age and wind mitigation | Licensed inspector | During inspection period |

| Insurance quote (NFIP vs. private) | Insurance broker | Before financing commitment |

Additional items deserve attention specific to coastal construction. Seawall integrity, roof age relative to hurricane exposure, and evidence of salt-air corrosion on structural elements all carry more weight here than in inland markets. A standard home inspection is a starting point, not a complete picture. Engage specialists in marine engineering and wind mitigation separately.

- Verify short-term rental zoning and any HOA restrictions before assuming rental income projections

- Confirm utility infrastructure capacity, particularly for properties on private wells or septic systems

- Review title history for any coastal setback violations or prior unpermitted work

- Check for any pending litigation involving the HOA or adjacent properties

Pro Tip: Commission a wind mitigation report early. It directly affects insurance premiums and can be used as a negotiating tool if the property needs upgrades.

What negotiation strategies work in Amelia Island's luxury market?

Negotiation in a thin, seasonal market requires a different posture than in high-volume suburban markets. When active listings in your target tier number fewer than ten properties, the leverage dynamic shifts toward sellers, particularly for well-located, well-maintained homes. Your strongest negotiating position comes from preparation: a fully underwritten loan approval, a clean offer structure, and a demonstrated understanding of micro-location comps.

Second-home and short-term rental investors create predictable supply swings that a knowledgeable buyer can use to their advantage. Properties that come to market in late summer or early fall, after the peak season, sometimes carry more seller flexibility. Conversely, a property that appears in March with strong rental income documentation will attract competitive interest quickly.

The role of a local luxury specialist cannot be overstated. An agent with deep knowledge of Amelia Island neighborhoods brings access to off-market inventory, regulatory nuance around short-term rental restrictions, and the relationship capital to negotiate with sellers who value discretion. A generalist agent working from county-level data is a liability in this segment, not an asset.

Practical negotiation approaches for this market:

- Lead with a clean offer: fewer contingencies, flexible closing timeline, and a meaningful earnest money deposit signal seriousness

- Use micro-location comps, not county medians, to anchor your price position in writing

- Request seller-paid flood insurance for the first year as a closing credit rather than a price reduction, which preserves the seller's net figure

- If a property has been on market more than 90 days, investigate the reason before assuming it represents leverage

- Factor in the cost of coastal ownership including insurance, HOA, and maintenance when modeling your total carrying cost

Understanding jumbo mortgage requirements early in the process also strengthens your negotiating position. Sellers in this tier have seen deals fall apart at financing, and a buyer who can demonstrate clean underwriting commands more credibility at the table.

Key takeaways

Succeeding in the $2M–$10M Amelia Island market requires micro-location knowledge, early flood insurance verification, and a local specialist who can access inventory before it reaches the public market.

| Point | Details |

|---|---|

| Use micro-location comps | Build comp sets by neighborhood type and water orientation, not ZIP code or county medians. |

| Verify flood risk early | Request the elevation certificate and insurance quotes before finalizing your offer. |

| Scrutinize HOA finances | In boutique communities, review three years of financials and confirm reserve fund adequacy. |

| Prepare financing in advance | A fully underwritten approval strengthens your offer in a thin, competitive market. |

| Work with a local specialist | Off-market inventory and regulatory knowledge require an agent with deep island relationships. |

What I've learned from watching buyers succeed and struggle here

I've watched buyers with significant resources make costly mistakes on Amelia Island, and the pattern is almost always the same. They arrived with a strong financial position and a general sense of what they wanted, but they underestimated how much this market rewards preparation and local knowledge over capital alone.

The micro-location insight is the one I return to most often. A buyer who anchors their valuation to Nassau County's median sale price of roughly $490,000 is operating with a framework that has almost no relevance to a $4M oceanfront estate. The island's luxury segment follows its own cadence, and understanding that cadence requires spending time in the market before you need to act in it.

Seasonal supply shifts are real and predictable, but they require buyer agility that most people underestimate. When a well-priced property appears in a thin market, the window to act is measured in days, not weeks. Buyers who have done their homework, toured comparable properties, and secured financing in advance are the ones who close. Those who are still gathering information when the listing appears typically lose it.

The due diligence piece is where I've seen the most last-minute financing issues. Flood insurance underwriting results can vary significantly based on elevation details and lender requirements, and discovering that variance at the closing table is an expensive lesson. Start the insurance conversation the moment you identify a property, not after you've signed a contract.

My honest recommendation is to use a local luxury specialist who works specifically in the $2M–$10M tier on Amelia Island. The difference in access, insight, and negotiating effectiveness is not marginal. It is the difference between seeing the full market and seeing only what reaches the public MLS.

— John Hillman

How Craneisland helps you find your place on Amelia Island

Craneisland sits at the intersection of luxury coastal living and genuine environmental stewardship, offering a rare collection of custom Intracoastal homesites on Amelia Island. With only 14 homesites available, each woven into preserved marshlands and framed by Lowcountry architecture, this is a community built for buyers who want more than a property. They want a legacy.

The Craneisland team brings deep knowledge of the $2M–$10M segment, from pricing dynamics to the design-build process for buyers who want to create something entirely their own. Whether you are exploring available homesites or considering a custom home design, we are here to walk you through every step with the care and expertise this market deserves. Reach out to begin a conversation about what life on Amelia Island can look like for you.

FAQ

What price range defines luxury real estate on Amelia Island?

The luxury segment on Amelia Island starts around $1M and extends well past $3M for oceanfront estates, with the $2M–$10M tier representing the most active band for discerning buyers and investors.

Why is Nassau County's median price misleading for luxury buyers?

Nassau County's median sale price near $490,250 reflects the full county market and significantly underrepresents the pricing dynamics of Amelia Island's luxury and oceanfront segment. Buyers should use micro-location comp sets instead.

How does flood insurance affect buying homes on Amelia Island?

Properties in FEMA Special Flood Hazard Areas require flood insurance, and lender requirements can substantially affect carrying costs. Reviewing the elevation certificate and comparing NFIP versus private insurance options early in the process is critical.

What makes boutique HOA communities riskier to buy into?

In communities with fewer than ten units, unexpected HOA costs divide among very few owners, making the per-unit financial impact disproportionately large. Always review three years of financials and confirm reserve fund adequacy before committing.

How do I access off-market luxury listings on Amelia Island?

Off-market transactions are common in the $5M–$10M tier, and access depends almost entirely on working with a local specialist who has established relationships within the island's luxury agent network. A generalist agent working from public MLS data alone will miss a meaningful share of available inventory.